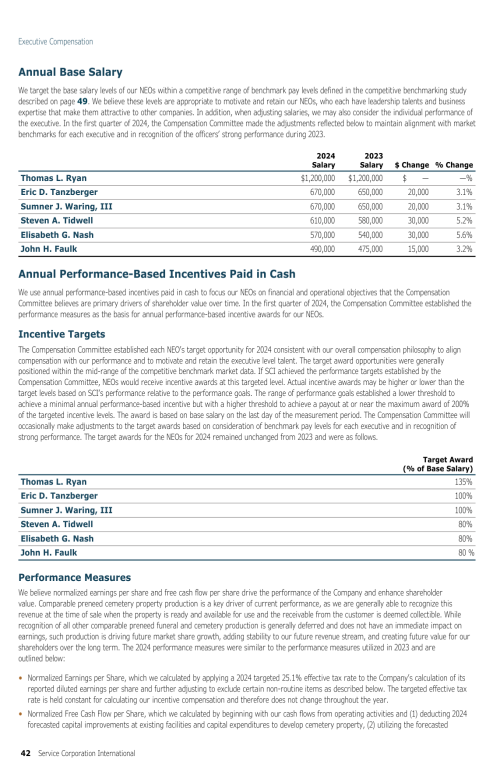

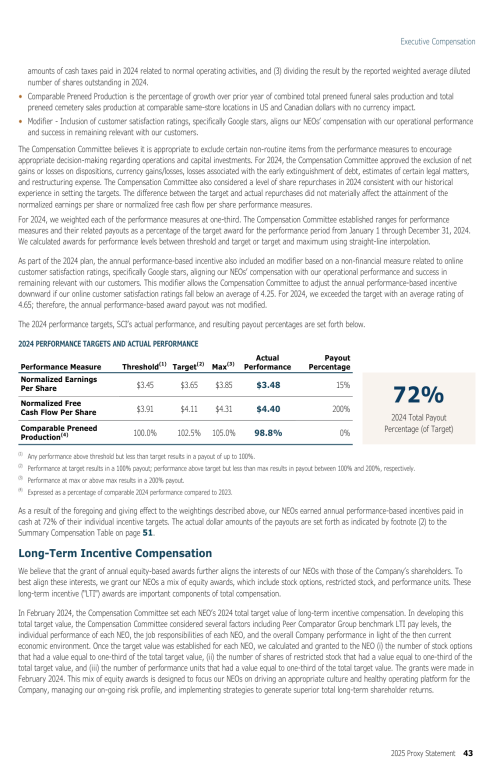

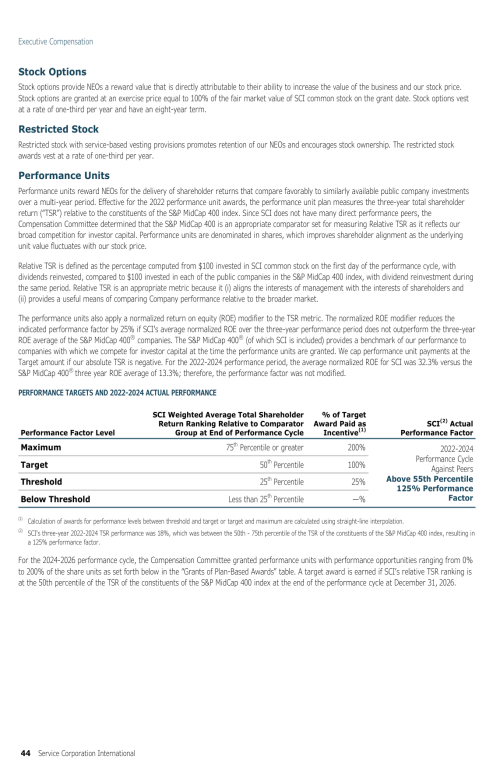

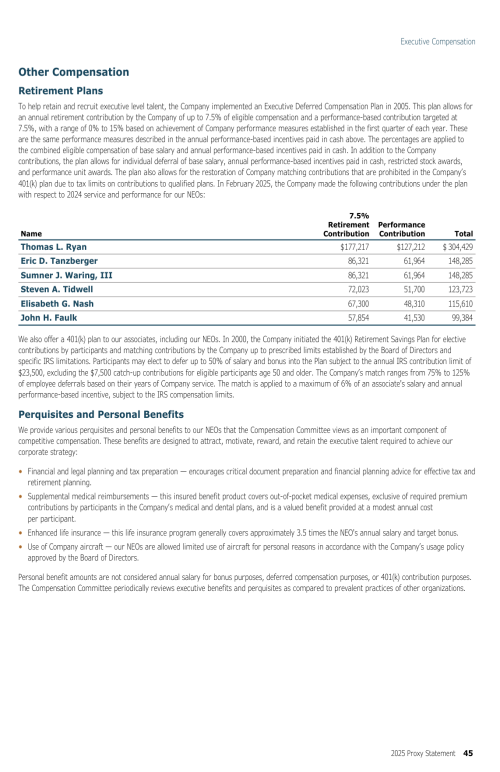

| Item | Voting Recommendation | Page |

|---|---|---|

| Election of 10 Directors | FOR each Director nominee | 6 |

| Ratify the Selection of Pricewaterhouse Coopers LLP, Our Independent Registered Public Accounting Firm | FOR | 12 |

| "Say-on-Pay" Advisory Vote to Approve Named Executive Officer Compensation | FOR | 13 |

© 2025 Service Corporation International